Insights from Innov8 Talks at IIJS Signature Bharat 2026

At a time when the global diamond industry is seeking direction after years of disruption, the Innov8 Talks at IIJS Signature Bharat 2026 delivered something the trade values most: clarity without comfort.

Rather than offering quick optimism or dramatic warnings, the session presented a grounded view of where the natural diamond market stands today—and what it must confront to remain relevant tomorrow.

The joint presentation brought together Prasad Kapre, Industry Analyst & Consultant at Blue Sky Business Management Group; Pranay Narvekar, Partner at Pharos Beam Consulting LLP; and Edahn Golan, CEO & Founder of Edahn Golan Diamond Research.

Well attended by a mixed audience of manufacturers, exporters and retailers, the session set a tone that was realistic, tough, and necessary.

Recovery Is Visible—But the Old Market Is Gone

One of the clearest messages from the session was that the diamond industry is not in decline, but it is no longer operating on familiar terms.

In the US—the world’s most influential consumer market—diamond jewellery demand is showing slow but steady improvement. However, this recovery is being driven by higher average spending per item, not by an increase in unit sales.

Consumers are buying fewer pieces, but they are prepared to spend more on the right ones.

What the data confirmed was not a collapse in interest, but a structural shift in behaviour. The post-pandemic surge has fully unwound, and consumption has returned to long-term trendlines rather than exceptional highs.

Key Market Signals Highlighted at Innov8 Talks

- US diamond jewellery demand showing gradual improvement

- Growth driven by value, not volume

- Rising average transaction sizes; declining unit sales

- Resilience in mid-to-higher price bands; pressure at entry level

- Industry stability expected by mid-2026, not a return to rapid growth

Why the Midstream Still Feels the Pressure

If retail demand is stabilising, why does the pipeline still feel strained?

The answer lies in the bullwhip effect—a familiar but often misunderstood dynamic in the diamond supply chain. Demand volatility at the consumer end becomes amplified as it moves upstream, meaning manufacturers, polishers and rough suppliers experience deeper and longer cycles of stress.

Retail typically recovers first. The midstream follows later.

This explains why polished exports and imports across major centres remain weak even as downstream indicators show improvement. Historically, this ripple takes close to a year to fully work its way through the industry.

The important distinction made during the session was this: pipeline pain is a lagging indicator, not a permanent condition.

Engagement Rings: Where Emotion Meets Economics

Few segments reflect the industry’s transition more clearly than engagement rings.

In mature markets such as the US, wedding numbers have plateaued. At the same time, younger consumers—particularly those aged 25 to 35—are increasingly price-oriented, less attached to traditional diamond narratives, and more open to alternatives.

Lab-grown diamonds have gained significant share in lower price points. Yet the session also highlighted an important counter-trend: many consumers remain willing to pay a premium for natural diamonds, provided they see clear emotional and symbolic value.

What became evident was that the challenge is no longer affordability alone—but identification.

Consumers want to understand what they are buying, and why it matters.

LGDs and Natural Diamonds: Coexistence Requires Clarity

Lab-grown diamonds were addressed not as a threat, but as a category that demands clear separation.

One of the most striking observations was that unchecked proliferation risks diluting the appeal of diamonds altogether. When access becomes universal without distinction, rarity loses meaning.

The consensus was not confrontation, but differentiation. Over time, lab-grown and natural diamonds will serve different purposes, speak to different motivations, and increasingly move through separate retail channels.

For this coexistence to work, differentiation must be intentional, transparent, and consistently communicated at the consumer level.

Stability Ahead—But Growth Cannot Be Assumed

Looking forward, the presenters projected that the natural diamond industry is likely to reach broad stability by mid-2026, with prices bottoming out earlier and market equilibrium improving in the second half of the year.

However, a key caution was repeated throughout the session:

stability does not necessarily mean growth.

Long-term demand for natural diamonds has narrowed structurally. Rapid expansion in a maturing market will inevitably come at the cost of margins.

External factors—tariffs, gold price volatility, and geopolitical friction—will continue to influence short-term outcomes. Yet these were presented as manageable and temporary, not existential threats.

The Question the Industry Can No Longer Avoid

Perhaps the most consequential part of the session was not about demand curves or price forecasts, but about stewardship.

For decades, category stewardship—the careful management of supply, messaging and long-term value—was effectively centralised. Today, with a fragmented market and no single player able to carry that responsibility alone, the industry faces a vacuum.

The long-term health of natural diamonds will depend on collective choices: production discipline, differentiation, and sustained category-level marketing.

From Luxury Product to Branded Category

This led to the session’s most compelling insight.

Natural diamonds are widely accepted as a luxury product. But they are not yet positioned as a luxury brand.

Without a unified narrative that reinforces rarity, emotional significance and long-term value, the category risks being defined primarily by price and comparison. Promoting “Only Natural Diamonds” as a distinct, aspirational proposition emerged as a central theme.

Keeping the “diamond dream” alive will require relevance—not nostalgia.

A Measured Path Forward

The Innov8 Talk did not offer easy answers, nor did it indulge in pessimism. Instead, it delivered strategic clarity.

The natural diamond industry is not fading—but it is being tested. Recovery is underway. Stability is in sight. Opportunity remains.

What happens next will depend on whether the industry chooses merely to adapt to change—or to actively shape its future.

What the Industry Needs to Get Right

- Clear differentiation between natural and lab-grown diamonds

- Repositioning natural diamonds as a branded luxury category

- Stronger emotional storytelling for younger consumers

- Collective responsibility for category marketing and stewardship

Related Coverage

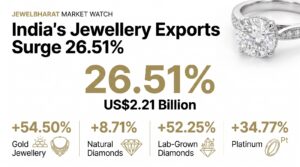

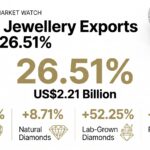

India’s Gem & Jewellery Exports Rebound 26.51% in June as Global Demand Strengthens

GJC and SGL Partner to Launch Dedicated Diamond Certification Pavilion at GJS Diwali Edition 2026

India–UK CETA Comes Alive as Mumbai Flags Off First Jewellery Export Consignment to the UK

India Opens Door to Global Diamond Auctions as Rapaport Debuts Pre-Auction Viewing in Mumbai

GJEPC’s IIGJ Lab Opens Collection Centre in Jaipur to Bring Trusted Gemstone Certification Closer to the Trade